'Cause Regulators Are Players Too

Wassup, party people. Today we’ve got a quick hit on (good) regulation, then another example of how crypto can work behind the scenes (AKA the “reverse crypto mullet”) and finally we wrap up our discussion on some advanced techniques for building the actual blocks of the blockchain.

We’ve also talked disproportionately about Tyler Hobbs’ unique art/NFTs in past issues, but yesterday a print of his Fidenza series sold at Chrstie’s for £290k. That’s chump change in the art world, but it was cool to see digital generative works sandwiched in a regular auction with pieces by Picasso, Pissaro, Renoir, Gaugin, Van Gogh, Calder, Hockney and Hirst.

🟢 Regulators Are People Too

(Big Idea: Regulation)

While the U.S. regulatory environment has focused on after the fact punishment, international regulators, particularly in the UK, have been engaging with crypto much more productively.

Earlier this month, the Bank of England and UK Treasury published a joint paper acknowledging the need for a digital pound (nee “BritCoin”) and committing to further preparatory work. Now, the very earliest they imagine a go/no go decision on if they even begin building is 2025/2026 so maybe don’t hold your breath, but it’s a good start at least and an encouraging sign that they are looking forward.

The outline imagines public-private partnerships featuring an API access that “allows private sector intermediaries to connect to the core ledger.” So, the BOE issues a digital version of the Pound (generally called a CBDC for “Central Bank Digital Currency”) that is convertible at any time into dollar dollar bills, y’all real world paper pounds. Private, regulated companies, presumably banks, but perhaps well beyond banks, would provide consumer access via digital wallets or other interfaces. The plans include a commitment to privacy, saying “privacy is fundamental to trust and confidence in the CBDC system.” But it also includes a proposed per user cap of £20,000 to limit exposure.

To their credit, the report demonstrates that the Bank of England understands the changing role of money. A decline of “public money” (i.e. cash), the rise of “private money” not issued by central banks (i.e. bank deposits and credit cards) and new innovations like crypto stablecoins.

Roughly a week earlier, the UK Treasury also released new proposals for how cryptoassets would be regulated. It acknowledges that crypto has many characteristics that make it very different from traditional securities and that the focus should be on regulating activities and disclosures instead of regulating the assets themselves. It includes minimum standards of information to be made available as well as liability for false and misleading statements.

Throw in a recent guide from a non-governmental, but highly influential, UK body endorsed by the Ministry of Justice on how to issue blockchain securities under English law and you see an altogether more future-looking environment across the pond. It certainly helps that the UK PM is 42 and graduated from an esteemed U.S. business school, but Rishi Sunak has publicly stated an ambition to make the UK a crypto and fintech hub and these are clearly good steps in that direction.

Meanwhile, the U.S. securities regulators are doubling down on a ruling on orange groves more than 75 years ago (Florida man strikes yet again!). Gary Gensler of the SEC has a new interview with New York magazine this week in which, amongst other things, he defends his two meetings with Sam Bankman-Fried. He explains that he was only there to set Bankman-Fried straight: “Gensler, in his telling, sharply rebuffed the group.” He goes on to indicate that “everything other than bitcoin” is a security in his estimation. Of course, to a hammer everything is a nail.

Many have questioned Gensler’s motivations, whether they be political (keeping his job and/or ascending to run the Treasury) or financial (he was at Goldman Sachs for 18 years before entering the political sphere). I found this Twitter thread interesting and a good jumping off point if you want to do deeper on Gensler, but it makes two larger points: 1) That this particular interview is a narrowly targeted PR strike by Gensler, making his anti-crypto case to the core of the Democratic party and, much more broadly, 2) that “the world of ownership is not going to become less digital.”

I remain convinced that crypto is not a set of technologies that will get put back in the box. I’m hopeful that we’ll see more models of productive regulation like in the UK, Switzerland or Singapore influence policy at home. We can align ourselves with democracies that support open access and freedom of choice or we can follow dictatorships that try to ban these technologies as a threat to their power.

🟦 Hybrid Custody

(Big Idea: Crypto Rails)

One of our biggest ongoing themes here is about how crypto will increasingly provide the rails of the Internet while its complexity and confusion can be hidden by smart intermediary layers. I’ve called this the “reverse crypto mullet™”: party in the front, crypto in the back.

An interesting example of this is the Flow blockchain. Flow is sort of a faux-blockchain. It has started out its life controlled by one company and is hardly decentralized, but it does this intentionally to improve the user experience and aims to decentralize over time. It is built by Dapper Labs, the company that launched CryptoKitties (which established ERC-721 as the standard for NFTs) and then created NBA TopShot.

Flow is working on a new way to manage user access in a method called “hybrid custody.” In the “real” world, unless you have gold bars buried in your basement, you probably don’t directly control any of your assets. Your bank or brokerage takes care of that for you. If you forget your Chase password, they can reset it for you. In the crypto world, at its core, all of this control shifts to the user. You don’t need a bank or an intermediary to hold or send your crypto. That has some powerful implications, but with great power comes great responsibility. There’s no Bitcoin helpdesk that you can call to get your private key back. Some people are more than willing to make that tradeoff, often with the help of tools like hardware wallets that give them some recoverability.

But for the masses, securely storing a 12 word seed phrase is a bit too much so instead, they migrate back to intermediaries like Coinbase to manage their coins for them. Coinbase holds all of their user’s Bitcoin in a big, secure, collection of piles somewhere, fundamentally not all that different from how Schwab stashes your Gamestop shares. That’s all well and good, but a) it doesn’t work great once you want to do stuff with your crypto outside of the Coinbase universe and b) it doesn’t work at all if you ended up at FTX and they lose your coins.

Hybrid custody, as you can guess, tries to do the best of both worlds. Users sign up through a regular application/website that has a traditional setup: user name + password, some way to do a password reset, etc. But instead of just pooling everything together in one big account held by the application, a separate “child” account is created onchain. The application/website itself remains the “parent” and can fully execute transactions on behalf of the child.

Sort of like a traditional trust fund for a child, at a certain point, the child can take control of the account (although this is not required here). Because the child account lives fully on-chain, it has the ability to move away from the original parent application/website at any point. The end user could move that address to a self-custodied wallet completely on their own, with no need to export assets (possibly triggering capital gains) or risk mishaps in a transfer.

Like many things in crypto (or really the world) it may not be quite as simple or secure as it sounds at first blush, but these sorts of hybrid solutions are the types of things I think we will see more and more of over the next five years.

◆ Building Building Blocks, Part 3

(Big Idea: How Blockchains Work)

And now, the dramatic conclusion to our series on how the actual blocks in blockchains are put together. Two issues ago, we talked about Bitcoin where miners basically pick what to include in a block by saying “SELECT * FROM waiting_transactions ORDER BY fees_offered.”

Then last issue, we got into some of the complications with Ethereum where things are much more powerful. Since you can do so much within a single block like borrow and repay money instantly, the “how” you assemble a block and the order of transactions within that block becomes massively important. Miners have learned how to extract value (Maximum Extractable Value or MEV) by arranging a block to their benefit, most commonly to the detriment of others who end up paying higher fees or getting worse execution.

But, of course, that is not the end of the story (or it only would have been two parts). Adopting a “if you can’t beat ‘em, join ‘em” strategy, tools like Flashbots have emerged to reclaim MEV. Instead of sending transactions to a public mempool where your transactions are visible to everyone and subject to front-running, users can instead send them to a private transaction pool. In this case, the MEV still exists, but now it can actually be managed and even auctioned off. Basically, “If you want to front-run my trade, give me a cut.”

“Searchers” come along, examining all of the transactions, looking for MEV opportunities. The searchers that participate can assemble a “bundle” of transactions, combining the private Flashbots transaction pool as well as the public mempool.

Once they have these bundles built, the next new innovation is that they placed a bid in a first price sealed bid auction for how much they are willing to pay to include that bundle in the next block. The miners/validators then build the actual block, fitting in as many of the highest paying bundles that they can.

Now, you’re like, “Wait, this just means the fees moved somewhere else down the line.” That is correct, but there’s a few benefits. The first is that this restores some order, liquidity and predictability to the system. As “MEV Wars” started to heat up, bots competing with each other would sometimes quickly inflate the price of gas and there could end up being lots of failed transactions and wasted fees.

Second, now that the value in a bundle has been identified, quantified and auctioned which means you can do something with it. Earlier this month, Flashbots announced MEV-Share, a program that pays originating users back a share of the MEV that their transactions generate. Users can also control how transaction information they reveal to searchers maintain privacy vs. optimizing their share of payment back.

The closest comparison to traditional markets is something along the lines of Payment for Order Flow. Wall St. market makers know that retail traders have a better risk/reward profile so they are willing to give up some profitability to pay to get those trades, the order flow, sent to them. Those payments (at least in theory) can then be used by retail brokerages to fund things like free trades for consumers.

In the crypto world, MEV is kind of a fact of life, a side effect of having an open, transparent network that allows a blockchain to work. But then we see a continued evolution of tools like Flashbots then get developed to ameliorate some of the impacts and balance out the negative externalities.

This Week's Burning Hot Take

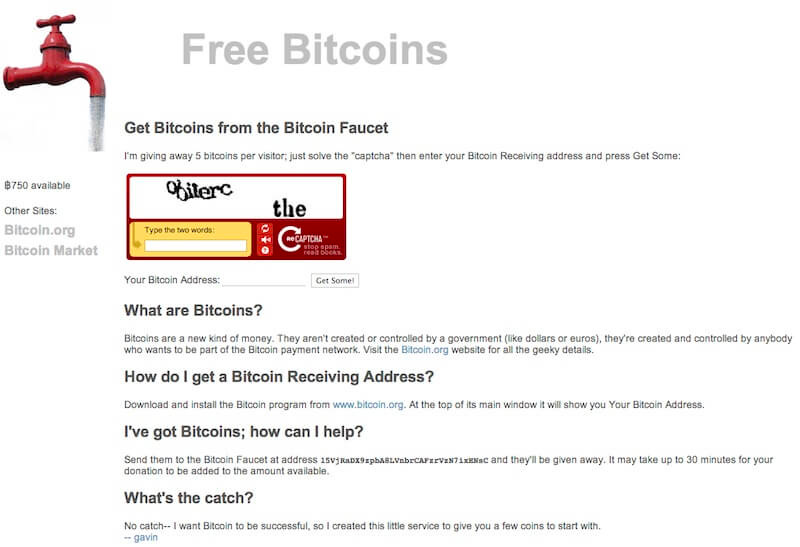

In 2010, Gavin Andresen was looking for a way to promote Bitcoin so he decided to give away 5 BTC per day to every user that came by. In total, the faucet gave away 19,700 Bitcoin in total, now worth nearly $500 million. Here’s what the site looked like way back then:

As always, thanks for reading. Send me questions and please share with your crypto curious friends.