The Messi of Fraud

Wait. What? You’re still here? I thought everyone bailed out of crypto two weeks ago. No? Cool, I appreciate you still being here.

Sadly, there’s more to unpack from the Bahamas, but if you’re sick of FTX and its ramifications, then feel free to skip ahead to the third section today. There we’ll discuss some of the fascinating possibilities that crypto enables to actually prove that your exchange actually has your money and isn’t using it to buy orgy palaces.

🟢 FTX Fallout

The basic outlines of what happened at FTX haven’t changed much in the last two weeks, but there’s certainly been lots of color around the scale and the depravity of it all. Some highlights:

FTX spent $300 million spent on real estate in the Bahamas, including a property worth $16.4 million in the names of SBF’s parents, both law professors at Stanford (Go Tree!).

FTX executives received loans including $1 billion (with a b) to SBF, $543 million to the head of engineering and $55 million to Ryan Salame (that dude must have sucked at his job to only get $55 mil).

Some perks that make olden-day Google look stingy: A “full suite of cars and gas covered for all employees [and] unlimited, full expense covered trips to any office globally.” And forget a jar of Kind bars, FTX US employees got $200 a day in DoorDash food delivery credits.

Expenses were approved over Slack using emojis.

On November 9, Ryan Miller, the general counsel of FTX US asked in a group chat, “Who can turn off the websites?” On November 10, he pleaded, “The exchanges must be halted immediately… The founding team is not currently in a cooperative posture.” On November 11, hours after finally filing for bankruptcy, he wanted his photo taken down, “Who can go to FTX.com and FTX US and remove the pictures and bios of the people under ‘about?’”

We knew SBF had donated $40 million to Democratic campaigns and was the #2 donor behind George Soros. We also knew that Ryan Salame (of the mere $55 million loan) donated $24 million to Republicans. Now, SBF he claims he “donated about the same amount to both parties,” but donated to Republicans using dark money. “And the reason, was not for regulatory reasons, it’s because reporters freak the f*&# out if you donate to a Republican because they’re all super liberal. And I didn’t want to have that fight so I just made all the Republican ones dark.”

Alameda, FTX’s trading arm, had no way to measure profitability or even how much money they had. According to the WSJ, “when colleagues at Alameda proposed setting up rigorous structures and systems for risk, compliance and accounting, Mr. Bankman-Fried was dismissive of the idea… He said such extensive controls could crimp Alameda’s activity and limit how fast the firm could move to place trades, the people said, reducing potential profit.”

If someone wired money into FTX, the wire instructions included a destination account owned by Alameda, because FTX hadn’t set up a bank account yet.

Here’s my summary to this point.

There were never any real lines between FTX and Alameda, despite being supposed completely independent companies. In fact, there were never any lines in any of it. There were over 100 entities that were all treated as personal fiefdoms, and money flowed in and out of those entities and into personal accounts on whims.

Alameda started out as a delta-neutral trader and probably made a bit of money in the early days. Delta-neutral usually involves lots of leverage to amp up returns which is theoretically tolerable if you are neutral. As more talented competitors moved into their space, they lost their edge and likely started losing lots of money. So instead, Alameda went long in what looked like a booming crypto market using their self-proclaimed “super powers.” Oh, and they left the leverage in place since that’s a good way to make even more money. Some evidence suggests that they had $22 billion in longs near the market peak.

When the markets turned in the Spring, those bets turned sour. Then Luna blew up and 3AC blew up and Alameda probably should have died then. But by that point they had most likely already used FTX customer funds so if they went down, then FTX would as well. So FTX propped them up with even more customer funds which they then proceeded to lose more of.

$8-10 billion in customer funds still remain missing. It’s unclear why SBF has not yet been arrested. Many think it has something to do with the approximately $100 million that has been donated across the political spectrum and some of the oddly soft press coverage he received even after the blowup. Yesterday he did an interview with the New York Timesy where he most deflected and pleaded ignorance. Then he got to go on Good Morning America this morning and continue to flood the zone with obfuscation.

The SEC has brought charges against an OpenSea product manager who made $20,000 front running NFT trades, but meanwhile SBF is chilling in the Bahamas, doing the grand tour of “ohh, it was just innocent incompetence” instead of a massive fraud.

Ben Thompson of Stratechery also had a good summation this morning:

“Assets held under these [FTX’s] terms can not, by definition, be subject to a bank run. A bank takes in deposits and lends them out; if too many people come calling for their deposit before the loans can be collected, the bank will run out of money — that’s a bank run. FTX, though, specifically promised customers that their funds would not be lent out. The fact that they were was fraud, and it is mystifying that so much of the media refuses to state what is, without question, a fact.”

🟦 The Virus Spreads

Two weeks ago, we expected there would be some contagion, but it hadn’t quite started yet. Now we’re seeing a bit more. 18 months ago, BlockFi raised a $350 million Series D at a $3 billion valuation. They filed for Chapter 11 on Monday. They idea was that you gave them your Bitcoin or other crypto and they would give you 6%-9.5% interest. Universally, people were like, “Wow, that’s an impressive yield.” From there, opinions bifurcated. For some, the next thought was, “Great, here’s my money. 6% is greater than 0%, duh.” Others were like, “Hmmm, Treasuries are earning 0.5% right now, where is this yield coming from?” Well, the answer was “wherever they could find it.”

Sure enough, BlockFi lent money to 3AC (a big crypto trading fund) which then lost it all. It’s still not clear quite how much BlockFi was down, but it was big enough that they needed some kind of a bail out. FTX came along to save them with a $400 million credit facility (of which BlockFi drew $275 million). At the time in July, people were like, “Oh, that’s so great that SBF is bailing out everyone in the space, he’s the new JP Morgan, but with better hair.” In retrospect, one suspicion is that BlockFi owned a large number of FTT tokens. If BlockFi was in trouble, they would dump the FTT tokens and the FTX fraud could unravel.

Yet by the time of the bankruptcy filing, BlockFi in fact was owed more than $1 billion from FTX/Alameda: a $671 million loan to Alameda and $355 million in funds frozen on FTX. Basically, the White Knight came in to fill the gap, but instead dug the hole even deeper.

Something similar happened with Voyager, another company offering the same thing as BlockFi. Voyager lost $600 million with 3AC and then, FTX “bailed them out” with a $500 million credit line. By the time Voyager filed for Chapter 11, Alameda owed them $377 million. And that was back in July when everything looked rosy (well, hardly rosy, but, you know, not like the day after Woodstock-y).

BlockFi doesn’t appear to be fraudulent. They were just an opaque, unregulated quasi-bank that took people’s money and lost it chasing yield. They even agreed to a $100 million fine from the SEC in the process of trying to get its lending product approved. [Ironically, they seemingly only paid $70 million of that fine and now the SEC is listed as a creditor in the bankruptcy filing for the other $30 mil.]

In the meantime, all eyes have been on Digital Currency Group, better known as DCG. DCG is one of the big boys of the industry: well funded with plenty of gray hairs with real financial experience. They’ve got at least five different business areas, but the two most notable are Genesis and Greyscale.

Grayscale runs the closest thing we have to crypto ETFs: a series of closed end funds that are intended to mimic the behavior of Bitcoin, Ethereum or other coins. There are two problems (depending on your perspective). The consumer problem (but strength for Greyscale) is that there is a 2% management fee just to hold the assets compared to public market ETFs where management fees can be under 0.10%. The bigger problem for everyone is that the price of the trust shares (which trade OTC) diverge massively from the underlying asset value. Currently, the value of all of the Bitcoin held in the GBTC trust is around $11 billion. But the value of GBTC is 42% less than that, a gap of almost $3.5 billion. We’ll cover this in future episodes, but this gap has been the root of much trouble for all types of investors over the years, likely exacerbating if not outright causing the 3AC collapse. Because closed end funds do have the same redemption/issuance mechanism and fluidity of ETFs, these NAV discounts can persist. But, from the Grayscale perspective, it’s a pretty good business clipping 2% coupons for just holding Bitcoin.

Genesis, on the other hand, is a big crypto lender. Probably the biggest and best regarded. But again, they lent to 3AC without sufficient (any?) collateral. When 3AC went under, Genesis may have lost up to $1.2 billion. Their exposure to FTX is still not fully known, but is also believed to be significant. They disclosed that at least $175 million of assets are locked/lost on FTX. Shortly after FTX fell apart, Genesis suspended redemptions and new loan originations. New reports suggest they are looking for a $1 billion emergency loan to avoid bankruptcy. The relationship between DCG and Genesis is tricky and it's not clear where the losses will fall, DCG at the corporate level may have the resources and cash flow to avoid Chapter 11. If not, expect more dominos to come tumbling down.

◆ Where Do We Go From Here

(Big Idea: Trustlessness)

OK, enough drama. Let’s try to get back to some of the real reasons that crypto is interesting and won’t disappear despite SBF’s best efforts to ruin it all.

For millennia, humans have relied on trusted third parties to facilitate transactions. When you give your money to a bank, they make a little notation in their table and you just kind of trust that they add the right amount and that the money will be there when you want to take it out. When you want to send someone money (via a check or a wire), you trust that the banks will talk to each other and correctly credit and debit everyone accordingly.

With crypto, the trust is built into the cryptography. You don’t have to trust, you can verify yourself. For example, you can see every Bitcoin transaction ever and if you can reach any Bitcoin node, you can send a transaction to any address without anyone’s permission and without trusting anyone else.

We talked not long ago about the concept of Zero Knowledge (ZK) proofs: “ZK proofs allow you to validate a piece of information without exposing any data to prove it. You basically “prove” something is true without doing anything more than verifying it is true.” An example might be proving that you are 21 years old without having to share your full birthday, home address or kidney donor preference.

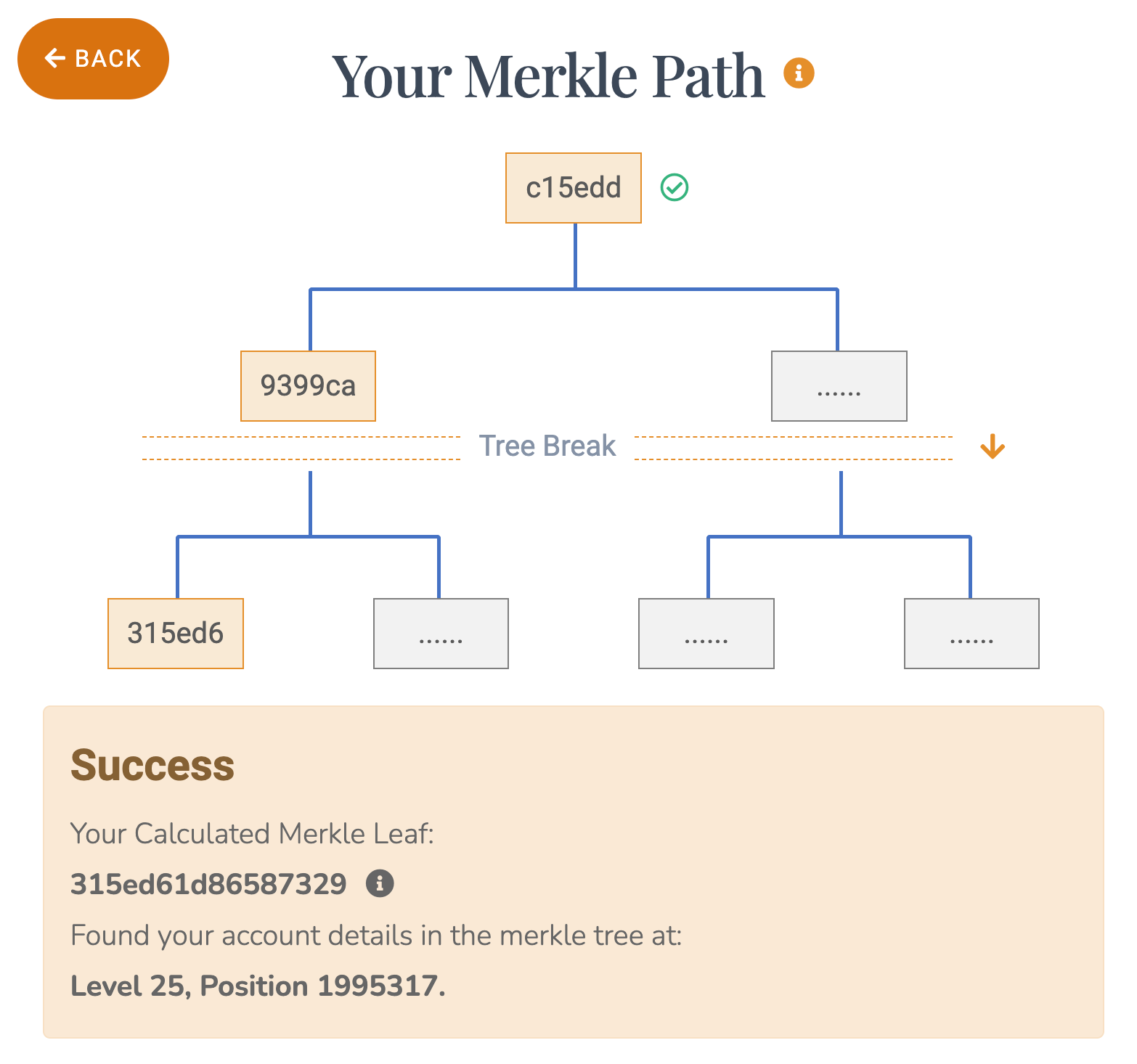

This concept has been much in the news since the FTX debacle in the form of Proof of Reserves (PoR). Proof of Reserves is a cryptographic audit that allows a custodian to demonstrate that they hold the assets that they claim while also allowing an individual user to verify their own assets within that structure. You can see, for example, how many Bitcoin an exchange holds and then also know that your personal Bitcoin are in that count.

For example, I currently use Kraken as my primary exchange, in large part because they were one of the first exchanges to offer Proof of Reserves. I can log in and see my place in a massive “tree” of accounts [Merkle roots are a very cool method of validating data integrity and are used throughout crypto, but explaining them is a bit beyond today’s scope.]:

Then I can go to the auditor and verify that my holdings are included in the total. The nature of the Merkle roots is that if a single character or number changes, every point higher on the tree will also change:

The Merkle tree preserves everyone else’s privacy and I can’t see their holdings, but I can be comfortable that, at least at the time of this snapshot, all of my assets are there and accounted for. It may have changed since then and this may not cover the liabilities side to prove that an exchange is fully solvent, but it goes a huge way to verifying trust. Nic Carter goes into more depth and also tracks the exchanges that have done a full PoR audit and the varying levels of audits possible.

Proof of Reserves also has important secondary effects/implications. If your exchange can put together a full PoR and make it through that kind of audit, it makes it more likely that they broadly have their sh*& together. FTX, for example, would have failed about 30 different places before even going down this path.

This Week's [Not Safe for Work, but Absolutely Hilarious] Freezing Cold Take

“If the price of Bitcoin doesn’t go to a million dollars by 2020, I will eat my own member.”

As always, thanks for reading. Send me questions and please share with your crypto curious friends.